The Asian Trilemma

Is the model that built Asia's miracle breaking?

Here is a question for you. Name the economies where exports account for more than half of GDP. Germany? No — 41%. China? No — 20%. The answers are Vietnam (90%), Cambodia and Malaysia (70%), Thailand (60%), and Singapore, which, at 175%, exports more than it produces, the economic equivalent of a magic trick. These are not merely export-oriented economies. They are the beating heart of globalization. Strip away the flows of goods, capital, and technology of the last five decades, and you strip away the Asian model itself.1

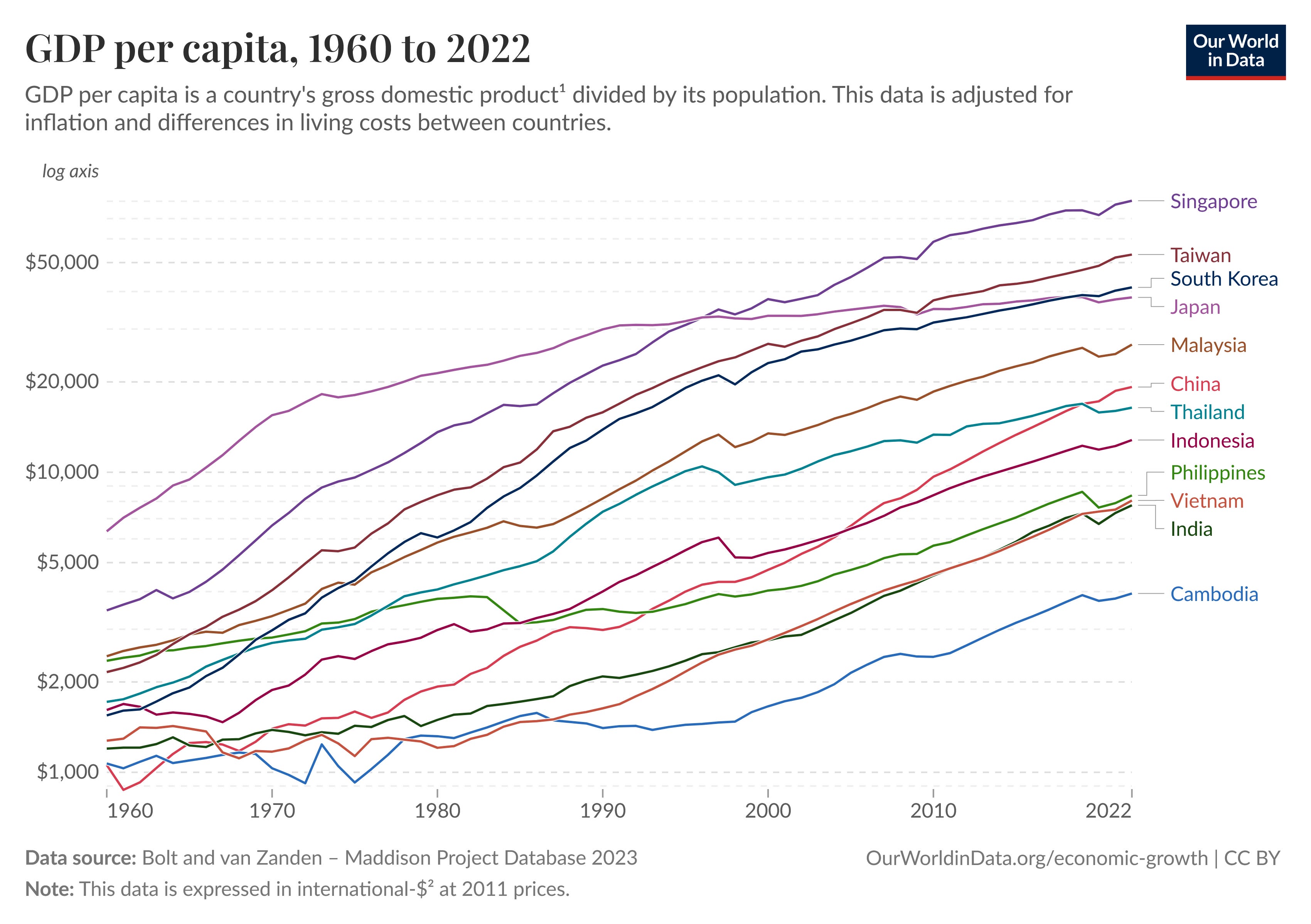

For fifty years, that model delivered the most compressed period of mass prosperity in human history. It rested on three pillars: open trade, a stable geopolitical order anchored by American power, and the assumption that technology would continue to flow from rich to poor countries, allowing catch-up growth. The Asian miracle was not an accident. It was facilitated and enabled by these three pillars (see below).

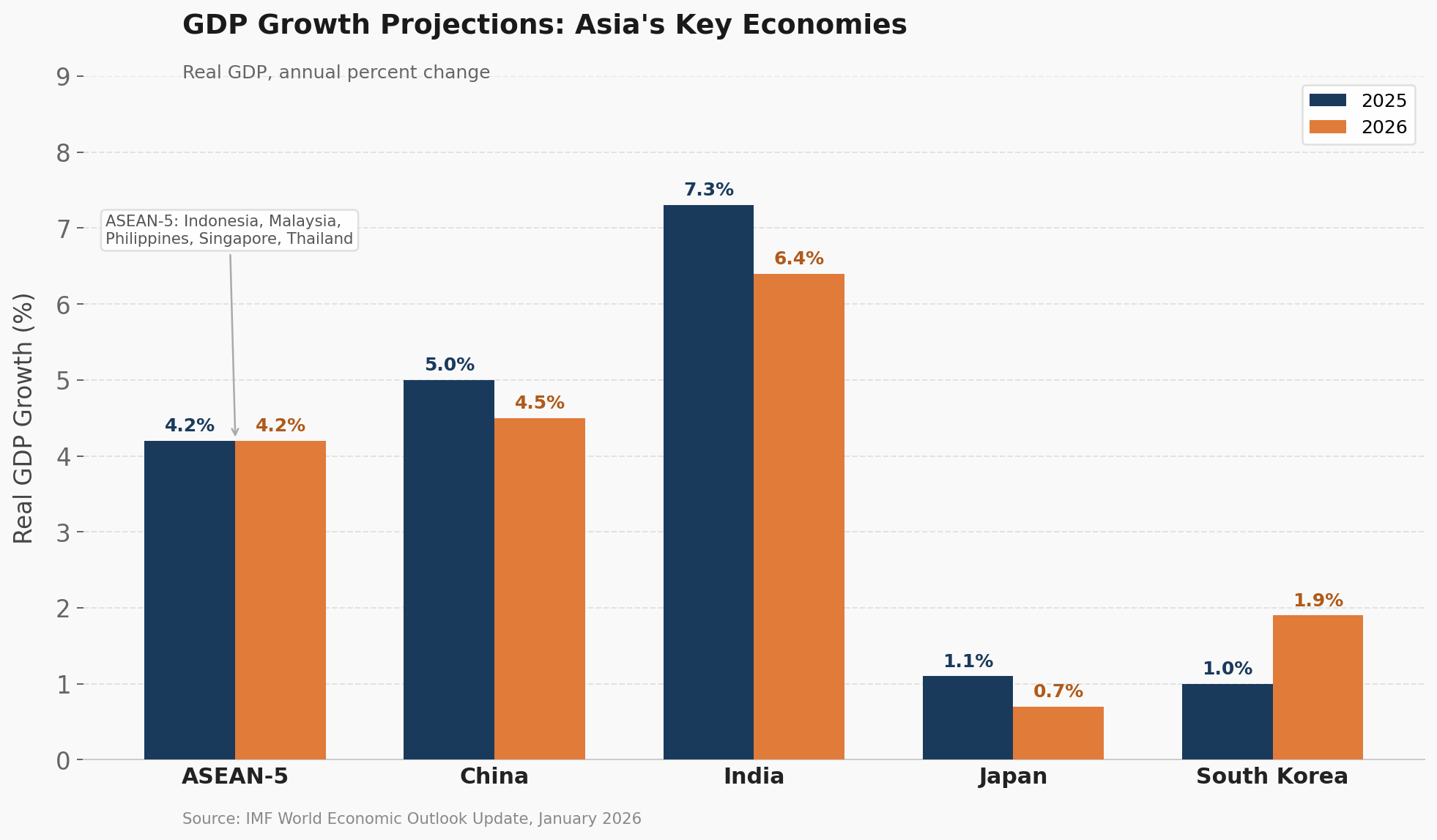

Unfortunately, all three are under strain as the world undergoes a structural break. The break is not yet visible in headline growth numbers (see below), which is precisely what makes it dangerous. The IMF projects most of Asia will grow respectably through 2026. But many factors that sustained GDP growth last year (tariff exemptions, TACO, stockpiling, the AI boom) may all wane in the years ahead, dragging growth down.

The Trade Pillar

Trump 1.0 was annoying but manageable. Tariffs were narrow, targeted, telegraphed in advance and phased in slowly. Crucially, firms could plan for them. Firms rerouted supply chains through Vietnam and Malaysia - the system bent but did not break. China plus one was the mantra chanted universally.

Trump 2.0 is different. The tariffs are sudden, volatile, whimsical, and coercive. The unpredictability is a feature, not a bug. Countries raced to strike deals: Vietnam accepted 20% tariffs in exchange for zero tariffs on its goods and commitments to buy American LNG and aircraft. Malaysia agreed to 19% and gave Washington a say over its export controls. Cambodia accepted coordination with the US entity list. Japan and Korea got 15% in exchange for investment pledges. Singapore, despite its free trade pact with the US, quietly accepted a 10% baseline tariff. Then, the Supreme Court stepped in and held these tariffs (IEEPA tariffs) as unconstitutional. Almost immediately, a 15% tariff on all countries under Section 122 kicked in. Interestingly, the discriminatory structure was flattened — everyone now gets 15%. The bilateral concessions, extracted under duress, and the trade deals are in limbo - some will be slow-walked, some renegotiated (India, EU), others reneged on.

For businesses, three tariff instruments are worth understanding. IEEPA tariffs - the ones Trump deployed first - are gone, replaced by Section 122 tariffs. However, even the latter are likely illegal, as they are used to address balance-of-payments issues that the US simply does not face. They expire in 150 days and what happens after that is anyone’s guess. Focus instead on the Section 301 tariffs - these are country-specific tariffs deployed after an investigation of unfair trade practices. They were the ones used against China in the first Trump administration. Another set in use is Section 232 tariffs, the instrument responsible for steel, aluminum, and the memorable suggestion that European cheese or Brazilian bananas were a threat to American defence. They are sector-specific and invoked on national security grounds. But the ones to truly fear and should keep lawyers and CFOs awake are Section 338 tariffs, last deployed in 1930. It allows 50% tariffs on a country-by-country basis, including embargos, and can be triggered by claims of regulatory discrimination, selective phytosanitary measures applied against US goods, or digital trade barriers. In a world where every economy practices some version of these, Section 338 is a loaded weapon pointed at everyone. Unused for nearly a century, lawyers are or should be rapidly familiarizing themselves with this section.

Beyond the tariff taxonomy, the more immediate threat is transhipment. Goods in Asian supply chains cross borders an average of six times before becoming a final product. Transhipment tariffs of 40%, designed to prevent rerouting and reclassification, expose Singapore, Vietnam, and Thailand to a compliance nightmare they are only beginning to map. The honest advice to a company today: invest heavily in data, trace what fraction of your inputs originate where, and prepare for rules that will change before the compliance systems are built.

Indonesia's position deserves a separate note. Its 2020 nickel ore export ban was a device to force Chinese and Western battery manufacturers to invest in downstream processing inside Indonesia rather than shipping raw ore abroad. They did not want to be an upstream commodity exporter, susceptible to the resource curse and the Dutch Disease. In fact, they wanted the entire value chain, from mining nickels to batteries to EVs. Indonesia holds roughly 22% of global nickel reserves and accounts for more than 60%of global nickel production. But here is the complication that the "Indonesia as China+1 alternative" narrative quietly ignores: Chinese firms currently control an estimated 70-80% of Indonesia's nickel processing capacity. The mineral is Indonesian; the value chain is largely not. Battery facilities have been slow to ramp up while Chinese EV manufacturers are shifting to battery chemistries that use far less nickel.

The Geopolitical Pillar

Japan and South Korea built their entire defence posture around one assumption: that the American security umbrella would be deployed in times of need. That assumption is now a question mark. The recent behaviour of the Trump administration — the Venezuela operation, the Greenland threats, the treatment of NATO allies as supplicants rather than partners — has communicated something specific to every Asian capital: sovereignty has a price, and the US no longer considers itself unconditionally bound by the architecture it built.

The Taiwan scenario concentrates this anxiety. A recent New York Times article put a number on what a Taiwan crisis would cost: an 11 percent decline in US GDP. China's economy would contract by 16 percent. Taiwan produces roughly 90 percent of the world's high-end chips and underpins an estimated $10 trillion of global GDP.

A full-scale crisis over Taiwan would not merely threaten TSMC. It would detonate the entire regional supply chain, including Singapore, Malaysia, Vietnam, Thailand, and the Philippines. ASEAN countries do not primarily buy from TSMC — they sit downstream of it, specializing in the assembly, testing, and packaging of chips before they reach final products. Malaysia is the world's largest chip exporter by volume; Singapore contributes roughly one in ten chips worldwide; the Philippines derives 62 to 65 percent of its merchandise exports from semiconductors. In 2024, Taiwan exported close to $40 billion in semiconductors and components to ASEAN, roughly 80 percent of which flowed to Singapore and Malaysia alone, which then re-exported them to end markets globally. Unlike the US, they have no domestic chip fabrication to fall back on.

What makes this especially uncomfortable is that ASEAN is exposed to the downside of both the current system and the transition away from it. A Taiwan crisis cuts off inputs. But a successful American reshoring effort (the Trump administration is pushing for 50 percent of chips to be made on US soil) also shrinks the flow of Taiwanese inputs through Asian ATP hubs.

The question ASEAN planners are not yet asking loudly enough is: what is our exposure not to a Taiwan invasion, but to a Taiwan disruption: elevated tensions before any shots are fired, when shipping insurance spikes, investment freezes, flows of chips are disrupted, and the great powers start asking smaller states whose side they are on? And, reshoring chip production to the US, which Trump seems determined to bring about.

The AI Technology Pillar

An AI Impact summit was organized in India just a few days back. The summit dismissed the “superintelligence soon" idea framing as an American imperialist narrative and instead bet on the diffusion of small models, open source models, and the need for some edge compute. There was talk of sovereign AI, regulations, and AI risk.

This may be right. But what if it happens to be wrong?

American hyperscalers — Microsoft, Google, Meta, and Amazon — collectively committed over $300 billion in AI capital expenditures in 2025 and have announced $ 690 billion in AI-related expenditures for 2026. The Stargate initiative alone is $500 billion over four years. These are investments in recursively self-improving systems and building “god in a box.” Again, it is right to question the fragility and the sustainability of this investment and lament the relentless hype of AI as a wizard. But then Claude Cowork and Code wiped out $300 billion in SaaS company valuations in a week!

Against this, Singapore's national AI strategy, which committed SGD 1 billion over 5 years, is a rounding error. This is not a criticism of Singapore; it simply cannot match these numbers. The question is whether "good enough" local models remain good enough as the frontier accelerates, or whether economies that made this bet find themselves locked into technological dependence on whoever controls frontier systems — almost certainly either the US or China — at precisely the moment when AI-driven productivity gains are widening the gap between frontier and non-frontier economies faster than any previous technology.

China is bringing on a different kind of pressure. Its relentless application of AI-enabled automation in manufacturing has compressed the low-cost labour advantage that Vietnam, Thailand, Indonesia, the Philippines, and India are counting on. Robot density in Chinese manufacturing rose from 25 per 10,000 workers in 2015 to roughly 392 in 2023 — nearly matching Germany, the most automated large manufacturing economy in the world, in under a decade. The window for labour-cost-based manufacturing competition may be closing faster than anyone in Jakarta or New Delhi is prepared to acknowledge.

India's position is the most paradoxical. Its $250 billion IT services sector, employing 5 million people, was built on one comparative advantage: large numbers of English-speaking engineers who could do, at lower cost, what Western firms needed. That advantage is being structurally eroded by the veryAI systems India now hopes to deploy for growth. And it is being built by the major AI companies, staffed and often led by Indians. The middle rung of the ladder is being pulled up while the climbers are still on it. TCS, Infosys, and Wipro are racing to reposition as AI integrators rather than code factories. The bet is plausible. But Cognizant and Infosys both cited 10-20% productivity gains from AI tools in recent earnings calls, suggesting the same work requires fewer people.

My fear is not that AI disrupts. Every technology disruptI fear is that the disruption arrives before the adaptation does, and that governments currently building five-year AI roadmaps premised on a plateau that may not materialise will look up in 2028 and find the world they planned for no longer exists. The hard question is what happens if deep, recursive learning proceeds at a furious pace. The likelihood of such a scenario has to be taken seriously. What institutions, policies and investments do countries need to genuinely engage with frontier developments? Otherwise, mouthing open source, small models, and sovereign AI is a coping mechanism and a form of denial.

In Closing

I know the convention. Every piece about Asia in crisis is supposed to end on a positive note. Every challenge is reframed as an opportunity. But sometimes a crisis is just a crisis. And compulsory or compulsive optimism is a form of denial.

The threats to Malaysia and Singapore in semiconductors, to Japan and South Korea on security, are real. So are the opportunities for India and Indonesia. The fracturing of the China-centric supply chain does create space. The demand for alternative manufacturing bases, alternative mineral suppliers, alternative technology partners — it is genuine. But the opportunity is narrow, time-bounded, and conditional on decisions that neither government has fully committed to: continued investment in logistics, reforms, and state capacity in India’s case, diversification away from Chinese processing dominance in Indonesia’s.

The Asian miracle was built on the assumption that the system would hold. The trilemma is the likelihood that it won’t. What is new for firms and governments in this region is that the pillars are cracking, and the pivot has to happen faster than the displacement. There is a fierce urgency of now.2

Of course, this is Southeast and Northeast Asia. India is relatively closed (export-to-GDP ratio is 21%).

What should firms do? That will be the next post.

Thoroughly enjoyed reading this very informative piece, thank you.